A “tick and flick” automated insurance quote is often the most expensive mistake an Australian investor can make. While a generic policy might satisfy a bank’s basic requirements, it rarely accounts for the complex realities of modern property management, such as evolving compliance requirements or specific rental market regulations that vary across jurisdictions. You likely understand the importance of protection, yet you might feel a lingering anxiety that your current rental property insurance leaves you exposed to tenant default or malicious damage. It’s a common frustration to feel like just another number in a digital system that prioritises speed over the actual security of your hard-earned asset.

At MyGen Insurance Brokers, we believe your peace of mind should be built on a foundation of precision rather than guesswork. This guide will show you how to move beyond basic coverage to secure a policy that actually performs when you need it most. We’ll explore the vital distinctions between standard home cover and specialist landlord protection, examine how current legislative and market shifts across the country impact your risk profile, and provide the expert clarity you need to navigate claims with confidence. By the end of this article, you’ll know exactly how to tailor your protection to suit the unique needs of your property.

Key Takeaways

- Understand the critical differences between standard home cover and specialist rental property insurance to ensure your investment isn’t left exposed to unique tenant-related risks.

- Learn why the $20 million public liability standard is a non-negotiable component of a robust policy, protecting your financial future from unforeseen accidents.

- Identify the hidden dangers of automated “sum insured” calculators that often lead to underinsurance in the current Australian construction market.

- Discover how to maintain your policy’s validity through methodical property inspections and regular maintenance to prevent common “wear and tear” claim exclusions.

- Explore the benefits of moving beyond generic, automated quotes toward a tailored protection strategy that accounts for the specific legislative requirements of your state.

What is Rental Property Insurance and Why Does it Matter?

Many Australian investors mistakenly view insurance as a static expense; a mere line item on an annual tax statement. However, true rental property insurance is a dynamic risk management strategy designed to protect the unique financial ecosystem of an investment property. It functions as a sophisticated shield that guards both your physical asset and your ongoing cash flow. While most people understand the basics of what is property insurance in a general sense, an investment requires a much deeper level of scrutiny. You aren’t just protecting bricks and mortar; you’re protecting a primary source of wealth and the legal responsibilities that come with being a housing provider.

We often describe this arrangement as “risk transfer.” Instead of holding the potential weight of a $60,000 malicious damage bill or a multi-million dollar legal claim on your own shoulders, you transfer that financial burden to a specialist insurer. This ensures that a single unfortunate event, whether it’s a natural disaster or a difficult tenancy, doesn’t derail your long-term financial goals. It is about moving from a position of vulnerability to one of professional certainty.

The Difference Between Home and Landlord Cover

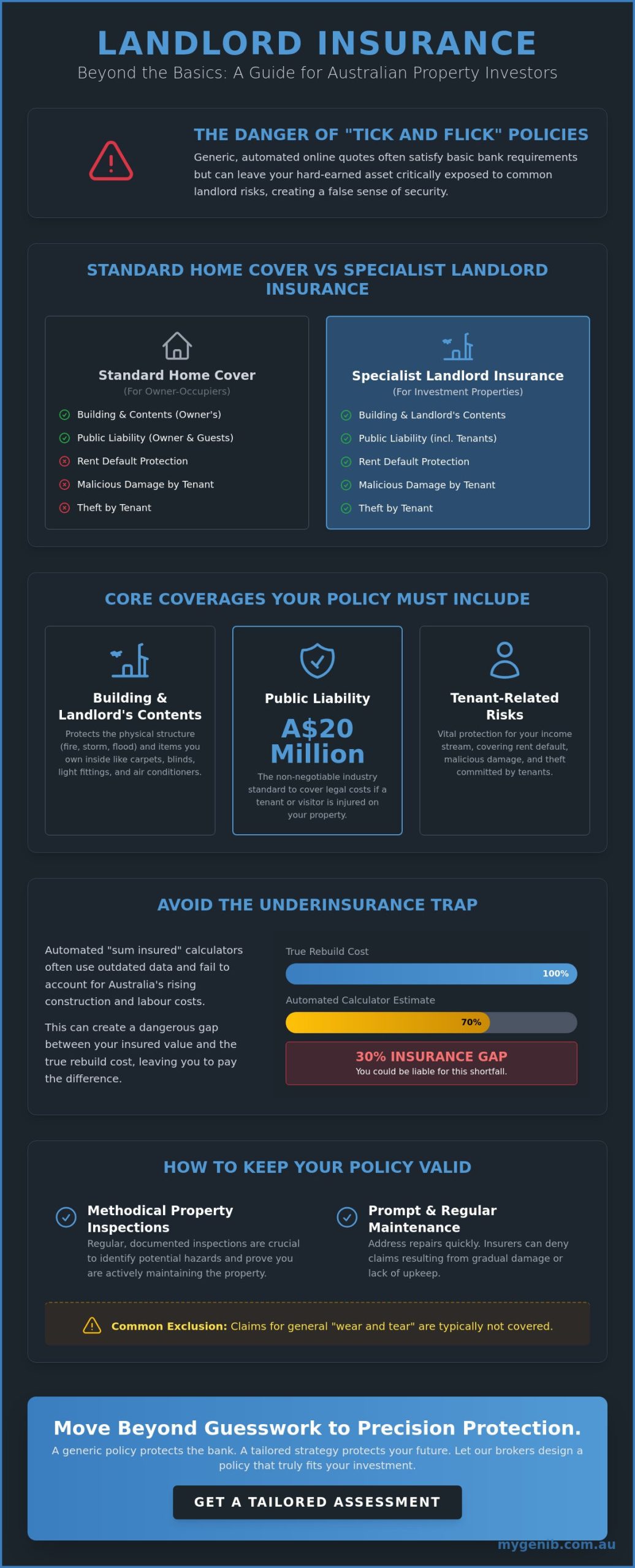

A common trap for new investors is assuming a standard homeowners policy will suffice. Most residential policies are built on the premise that the owner occupies the home. Once you invite tenants into the property, the risk profile changes entirely. Your standard home policy likely excludes tenant-related incidents, leaving you exposed to significant gaps. Specialist rental property insurance bridges this gap by providing specific cover for rent default, theft by tenants, and the unique legal liabilities that arise when you’re responsible for the safety of someone else’s home. Whether you’re managing a long-term lease in a Brisbane suburb or a short-stay apartment in Hobart, the policy must reflect the actual usage of the building to remain valid.

Why Investors Can’t Afford to Self-Insure

Some investors consider “self-insuring” by setting aside a small contingency fund. In the current Australian property market, this is a precarious gamble. The reality of litigation costs and the rising price of building materials means that a single major incident can instantly wipe out years of rental yield. If a tenant is injured on-site and pursues legal action, the costs can be astronomical. Professional insurance placement provides a stabilizing force, ensuring that your investment remains a profitable asset rather than a sudden financial liability. True peace of mind comes from knowing that your hard-earned equity is protected by a policy designed to perform under pressure.

Core Coverages: What Should Your Policy Include?

A robust policy is more than a safety net; it’s a precisely engineered set of protections that accounts for the physical and financial vulnerabilities of your investment. At its foundation, rental property insurance must cover the building’s structure against major events like fire, storm, and flood. However, we often see investors overlook the “contents” portion of their policy. Even in an unfurnished house, you likely own the carpets, curtains, light fittings, and split-system air conditioners. These items are frequently excluded from a building-only policy, yet they’re the most likely to be damaged during a tenancy. Ensuring these assets are explicitly listed provides the first layer of professional security for your property.

Public liability is the second, and perhaps most critical, pillar of protection. In the Australian market, a A$20 million limit has become the non-negotiable standard. This isn’t just a random figure; it reflects the potential cost of legal fees and compensation if someone is injured on your premises. Understanding your landlord’s legal responsibilities is essential, as the courts often place a high burden of care on property owners. If a tenant trips on a loose floorboard or a visitor is injured by a faulty gate, you need the certainty that your insurer will step in to manage the litigation and settlement costs.

Protecting Your Monthly Income Stream

We believe the true value of rental property insurance is found in its ability to protect your cash flow when the unexpected occurs. Loss of rent cover shouldn’t just trigger when the building is burnt down. A high-quality policy provides relief in more common, high-friction scenarios:

- Tenant Default: When a tenant stops paying rent and you’re forced to go through the tribunal process.

- Hardship: Situations where a court releases a tenant from their lease due to personal circumstances.

- Prevention of Access: Crucial for strata properties, this covers your income if an event nearby prevents tenants from entering the building, even if your specific unit is undamaged.

Legal Liability and Professional Protection

The legal landscape for landlords is becoming increasingly complex. While some budget policies offer A$10 million in liability, we’ve seen that this often falls short when multiple parties are involved in a claim. You need a policy that doesn’t just pay out a settlement but also covers the professional legal expenses required to defend your position. This proactive support is vital when you’re dealing with the stress of a claim. If you’re unsure whether your current limits are sufficient for your specific risk profile, seeking tailored landlord insurance solutions can help clarify your position. It’s about ensuring that a single legal dispute doesn’t compromise the equity you’ve spent years building.

The Protection Gap: Why “Cheap” Online Quotes Can Be Costly

The allure of a small online discount or a sixty-second quote is hard to ignore. Yet, these automated algorithms are designed for speed, not suitability. When you rely on a “tick and flick” system, you’re trusting a generic script to understand the nuances of your investment. This approach often results in a significant protection gap where the policy exists on paper but fails at the point of claim. Genuine rental property insurance requires a more methodical investigation than a simple web form can provide. We believe that looking beneath the surface of a policy is the only way to ensure it actually performs when you need it most.

Generic providers often keep premiums artificially low by stripping away essential layers of cover. They rely on the fact that most investors won’t read the hundreds of pages in a Product Disclosure Statement until it’s too late. This creates a false sense of security that can vanish the moment a complex tenant issue arises. Moving from a generic transaction to a tailored placement is the difference between having a policy and having true protection.

The Risk of Underinsurance

One of the most pervasive dangers in the Australian market is the underestimation of “Sum Insured” values. Automated calculators frequently lag behind the real-world inflation of construction costs, demolition fees, and debris removal. If your property is underinsured, you may encounter an “Average” or “Co-insurance” clause. This means that if you’ve only insured your building for 80% of its true replacement value, the insurer may only pay out 80% of even a partial claim, leaving you to find the difference. To combat this, a professional broker manually reviews current local rebuild costs and site-specific factors to ensure your coverage reflects reality rather than an outdated estimate. For a broader look at how these policies function, this comprehensive guide to landlord insurance provides excellent context on the Australian landscape.

Exclusions You Need to Know

Budget policies frequently hide broad exclusions that catch investors off guard. You might assume your rental property insurance covers all water damage, only to discover that “gradual” leaks from a shower recess are excluded, unlike a sudden burst pipe. Similarly, pet damage or accidental breakages are often omitted from basic digital products. Perhaps most concerning is the “60-day vacancy” rule, which can automatically void your cover if the property remains empty between tenancies for too long. We take the time to navigate the PDS on your behalf, identifying these hurdles before they become a financial crisis.

Managing Your Property Risk: A Landlord’s Strategy

Securing a policy is only half the battle. To ensure your rental property insurance remains a valid and effective tool, you must adopt a proactive risk management strategy. Most insurers include clauses that require you to maintain the property in good repair. If a claim arises from a long-term maintenance failure, such as a rusted gutter causing internal water damage, the insurer may classify it as “wear and tear” and deny the claim. Regular, documented maintenance is your best defence against these common exclusions. It’s about demonstrating that you’ve taken reasonable steps to protect your asset from predictable decay.

Tenant selection is equally vital. While we provide the financial safety net, a thorough screening process is your first line of protection. This includes verifying employment, checking national tenancy databases, and ensuring the lease documentation is legally sound. We also recommend keeping a precise inventory of all landlord-owned contents, from the dishwasher to the outdoor furniture. This list, backed by dated photographs, simplifies the claims process and removes any ambiguity about what was in the property at the start of the tenancy. It transforms a potentially contentious claim into a simple, evidence-based transaction.

The Importance of Documentation

Entry condition reports are your most powerful evidence during a claim. These documents provide a clear baseline of the property’s state, making it difficult for a tenant to dispute liability for malicious damage. We suggest storing digital copies of every repair invoice and all communication with tenants in a centralised, secure system. Additionally, you should review your “Sum Insured” annually. As Australian property values and construction costs fluctuate, your coverage must evolve to prevent the underinsurance traps we discussed in the previous section. A policy that was sufficient two years ago may leave you significantly short in today’s market.

Working with Your Property Manager

A professional property manager is a key ally in your risk management strategy, but their role must be clearly defined. While they often handle the initial reporting of an incident, the responsibility for navigating the insurance claim usually falls on the policyholder or their broker. It is essential to ensure your manager understands the specific requirements of your rental property insurance policy, such as the frequency of inspections required to maintain cover. We collaborate closely with your property management team, providing the expert guidance needed to align their on-ground actions with your policy’s fine print. If you want to ensure your management team and your insurance are perfectly in sync, we invite you to contact us for a professional policy review.

The MyGen Approach: Tailored Protection, Not Just a Policy

Traditional insurance often feels like a faceless transaction. Large corporations typically focus on volume and speed, but we believe that rental property insurance requires a more diligent, human-centric approach. We don’t just process policies; we investigate the specific risks of your property to ensure the coverage is genuinely suitable. This philosophy of looking beneath the surface allows us to identify the gaps that automated “tick and flick” systems frequently miss. It’s about moving away from superficial quotes toward a state of professional certainty.

A personalised consultation is the most effective way to turn a complex, high-friction experience into one that feels managed and secure. We take the time to understand your long-term goals, whether you’re a first-time investor or managing a diverse portfolio. We reject the “one size fits all” model in favour of a style that feels deeply personal and protective. This isn’t about finding the cheapest premium; it’s about building a protective framework that stands up to the rigours of the Australian rental market and provides genuine relief when things go wrong.

Your Advocate in the Claims Process

The true test of any policy is the claims process. When a tenant defaults or a major storm occurs, the financial and emotional stress can be overwhelming. We act as your steady, experienced hand, providing step-by-step support from the initial lodgement through to the final settlement. If a claim is disputed or complex, you don’t have to navigate the insurer’s bureaucracy alone. We act as your professional advocate, leveraging our industry expertise to ensure you receive a fair and timely outcome. This partnership provides the peace of mind that comes from knowing someone is doing the heavy lifting on your behalf.

Secure Your Investment Today

Starting the consultative process is straightforward and methodical. To provide a thorough risk review, we typically look at your current lease agreements, recent property inspection reports, and any existing policy schedules. This allows us to map out a strategy that addresses the specific legislative requirements and market conditions of your property’s location. We’re committed to building a long-term relationship based on accuracy and integrity rather than quick, generic transactions. We see ourselves as protective mentors, guiding you through every possible scenario to ensure your asset remains secure.

Your investment deserves more than a generic digital product. We invite you to organise a personalised landlord insurance review with MyGen Insurance Brokers to ensure your monthly income remains protected by rental property insurance that actually performs when you need it.

Secure Your Investment Legacy with Precision

Navigating the Australian property market requires more than just luck; it demands a deliberate strategy to protect your financial future. We’ve explored how moving beyond generic, automated quotes can reveal hidden exclusions and why a proactive maintenance plan is your best defence against claim denials. True rental property insurance isn’t a commodity you simply buy online; it’s a partnership designed to safeguard your monthly income and long-term equity from the unpredictable nature of tenancies.

Anthony Simpson and our team bring over 20 years of industry experience to every consultation, ensuring your portfolio is protected by a steady, experienced hand. We pride ourselves on a personalised approach that looks deeper than any algorithm, allowing us to build a policy that reflects the unique risks of your property. If a crisis occurs, we act as your dedicated advocate during the claims process to ensure you receive a fair and transparent outcome. We believe that professional protection is the foundation of every successful investment journey.

Contact MyGen Insurance Brokers for a tailored rental property insurance review today. Your hard-earned asset deserves the clarity and security that only a specialist broker can provide.

Frequently Asked Questions

Is rental property insurance tax-deductible in Australia?

Yes, the cost of your premium is generally tax-deductible in Australia when the property is rented or available for rent. The Australian Taxation Office allows you to claim this as an operating expense against your rental income. You should consult with a qualified accountant regarding the new ATO Ruling TR 2026/1, especially if your property has any private or holiday use, to ensure your deductions remain compliant with current tax laws.

What is the difference between landlord insurance and building insurance?

Building insurance focuses on the physical structure against events like fire or storm, whereas landlord insurance is a specialist form of protection that includes tenant-related risks. It bridges the gap by covering rent default, malicious damage by occupants, and the specific legal liabilities of being a property owner. While building cover is the foundation, a landlord policy provides the financial shield necessary to manage the unique complexities of a tenanted investment.

Does rental property insurance cover a tenant who stops paying rent?

Most comprehensive rental property insurance policies include cover for rent default, but it’s rarely a standard inclusion in budget “tick and flick” products. This protection triggers when a tenant stops paying rent and you’re forced to pursue an eviction through a tribunal. It’s designed to protect your cash flow during the often lengthy process of regaining possession and finding a new occupant, ensuring a single difficult tenancy doesn’t derail your mortgage repayments.

Am I covered if my rental property is vacant for a long period?

Standard policies often contain a “vacancy clause” that limits or removes cover if the property is empty for more than 60 consecutive days. If you’re undertaking major renovations or struggling to find a tenant in a quiet market, you must notify your broker to arrange an extension or a specific unoccupied property policy. Failing to disclose a long-term vacancy is one of the most common reasons for a claim denial in the Australian market.

What happens if my tenant causes malicious damage to the property?

If a tenant causes malicious damage, a specialist landlord policy provides the funds to repair the building and replace damaged contents like carpets or curtains. This is distinct from accidental damage or “wear and tear,” which insurers typically exclude. To ensure a smooth claim, you’ll need a thorough entry condition report and evidence of regular inspections to prove the damage was intentional and occurred during the period of insurance cover.

Do I need separate contents insurance if the property is unfurnished?

Yes, you still need contents cover because items like carpets, curtains, light fittings, and split-system air conditioners are not considered part of the “building” by most insurers. Even in an unfurnished house, these assets represent a significant financial investment. Including a specific contents sum in your policy ensures that you aren’t left out of pocket if a tenant damages these fixtures or if they’re destroyed during a major insured event like a fire.

How much public liability insurance do I need for a rental property?

A$20 million is the current industry standard in Australia for property investors. This high limit reflects the potential costs of legal fees and court-awarded compensation if a tenant or visitor is injured on your premises. While some older policies might only offer A$10 million, the rising costs of litigation mean that a lower limit could leave your personal assets at risk if a major claim exceeds your level of cover.

Can I get insurance for a short-term holiday rental like an Airbnb?

Short-term holiday rentals require a specialised policy that accounts for the high turnover of guests and the unique risks of platforms like Airbnb. Standard long-term rental property insurance often excludes stays shorter than 90 days or requires a formal residential tenancy agreement to be in place. We can help you navigate these specific requirements to ensure you have suitable protection for your holiday home, including cover for guest-related theft and liability.

Leave a Reply