What if the “instant” quote you just clicked through is actually a blueprint for a future rejected claim? With home insurance premiums on the rise across Australia, the pressure to find a comprehensive yet affordable deal is real, yet the risk of “ticking and flicking” your way into underinsurance has never been higher. We at MyGen Insurance Brokers understand the frustration of feeling like just another number in an automated system. Partnering with a dedicated home insurance broker Sydney families, and indeed families nationwide, rely on means moving away from generic algorithms and toward a strategy built on precision. It’s about ensuring that when you sign a policy, you aren’t just buying a document; you’re securing a promise that holds up when things go wrong.

We believe you deserve more than the confusion of fine print or the gap between market value and actual replacement costs. This guide will show you how MyGen Insurance Brokers can help you build a personalised safety net that accounts for the true rebuild price of your most valuable asset. We’ll examine why generic online calculators often fail and how professional human oversight provides the certainty you need. From understanding shifting commission structures to navigating the nuances of different cover types, you’ll discover how to transform a complex, high-friction chore into a source of genuine peace of mind.

Key Takeaways

- Move beyond the “tick and flick” culture of automated quotes to understand why speed is often the enemy of a truly accurate insurance policy.

- Identify the critical distinctions between building and contents cover, ensuring you aren’t caught out by the “grey areas” of carpets, curtains, and outdoor fixtures.

- Protect yourself from the underinsurance trap by learning how to align your policy with 2026 Australian construction costs and labour shortages.

- Discover how a home insurance broker sydney residents rely on can uncover exclusive market options and conduct a thorough investigation of the fine print in your policy documents.

- Transition from a generic transaction to a personalised safety net by prioritising professional accuracy and human oversight over superficial online calculators.

The Evolution of Home Insurance: Moving Beyond the Tick and Flick Culture

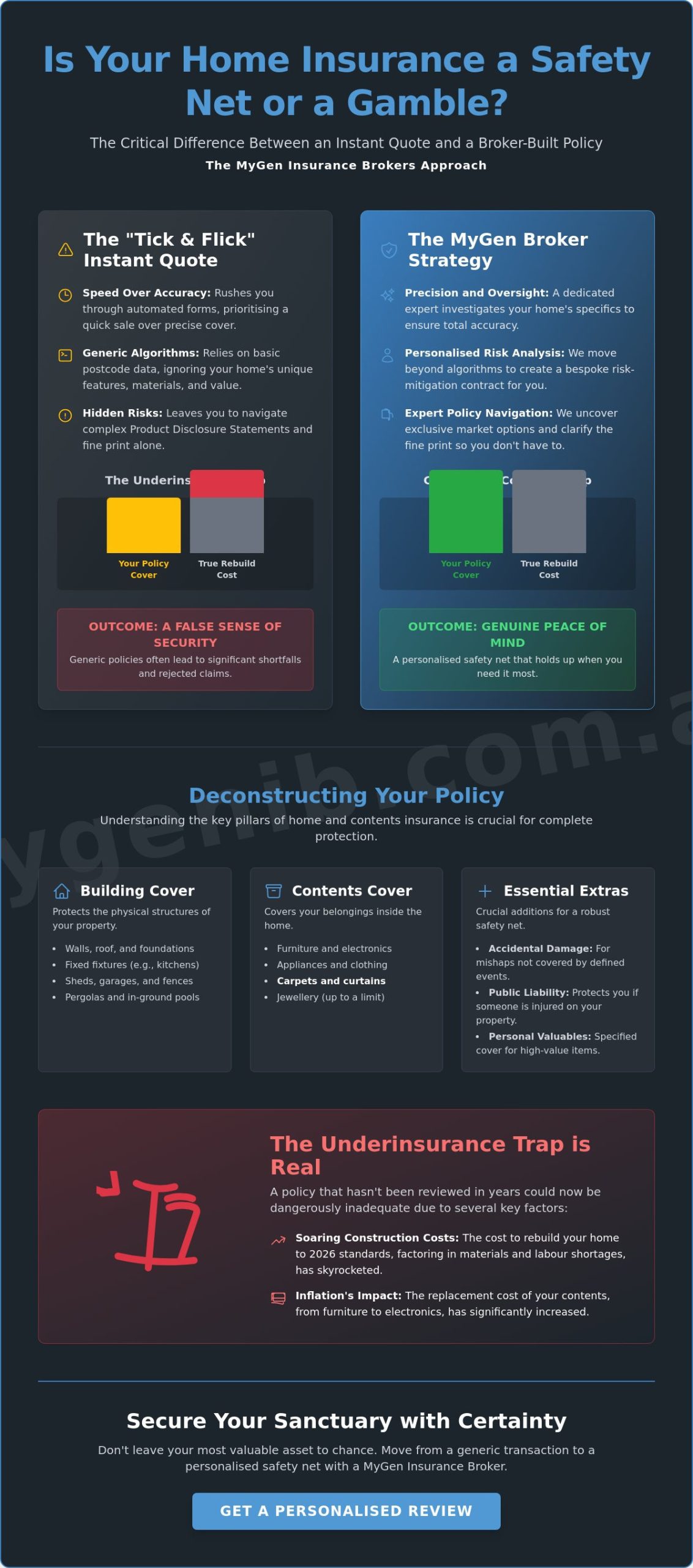

Your home is far more than a simple financial asset; it’s the structural shield for your family and the soul of your daily life. While most people view home insurance as a mandatory box to tick, we see it as a vital financial safeguard designed to protect that sanctuary. The modern insurance market has unfortunately shifted toward a “tick and flick” culture, where speed and low-cost premiums are prioritised over the accuracy of the underlying cover. This rush to complete automated online forms often leaves homeowners vulnerable, as generic algorithms cannot capture the specific nuances of a unique Australian property.

Adopting a “set and forget” mentality is a significant risk in the current economic climate. As the landscape of Insurance in Australia continues to evolve, relying on a policy you haven’t reviewed in years can lead to devastating coverage gaps. Inflation, rising building costs, and changes in local regulations mean that a policy which seemed adequate three years ago might now leave you hundreds of thousands of dollars short during a total loss claim. We believe in a consultative approach to domestic risk management, where we move beyond the transaction to understand the actual life lived within your walls.

Why Your Home is More Than Just a Postcode

Insurers often rely heavily on geographic data to determine risk, but your property is more than just a coordinate on a map. A home insurance broker sydney residents trust will look beneath the surface of simple postcode data. We consider the specific construction materials used, the age of the plumbing, and local environmental factors like proximity to bushland or flood zones. Generic policies frequently fail to account for unique features such as heritage architecture, custom cabinetry, or expensive solar installations. By investigating these details, we ensure your safety net is actually large enough to catch you.

The Shift from Transactional to Personalised Protection

There is a stark difference between the “call centre” experience and a dedicated brokerage relationship. When you rely on an automated system, you’re often left to navigate complex Product Disclosure Statements alone. Professional oversight acts as a calming, stabilising force, especially during stressful renewal periods or the high-stakes environment of a claim. We define homeowners insurance as a bespoke risk-mitigation contract tailored to individual asset profiles. It’s about moving from a state of anxiety to a state of certainty. Instead of being a faceless number in a database, you gain a protective mentor who does the heavy lifting to secure your future. This human-centric approach ensures that your policy reflects the reality of your life, not just a set of standardised assumptions.

Deconstructing the Policy: Building, Contents, and the Nuances of Coverage

Most policyholders assume their cover is a simple blanket. In reality, it’s a complex weave of three primary pillars: Building, Contents, and Personal Valuables. Understanding the boundaries between these isn’t always intuitive. For instance, many people are surprised to learn that while a wall is part of the building, the carpet attached to the floor is often classified as contents. These grey areas, including curtains and outdoor fixtures like pergolas, are where generic online quotes often fail. Navigating these definitions requires a steady hand. A home insurance broker sydney residents rely on will perform a deep dive into your specific property layout to prevent these common misunderstandings from becoming expensive mistakes.

Choosing between “Accidental Damage” and “Defined Events” is another critical fork in the road. Defined events only cover specific mishaps like fire or storm. Accidental damage is broader, protecting you against those “whoops” moments, like spilling red wine on a white sofa or a child knocking over a television. We also look closely at Liability cover, which acts as a financial buffer if someone is injured on your property. It’s an often overlooked but essential component of a robust insurance home and contents policy. While some agencies simply list building and contents as separate line items, they rarely explain the friction that occurs when a claim involves a “grey area” item. Is a split-system air conditioner a fixture or a piece of content? The answer varies between insurers and can determine whether your claim is paid or denied.

Building Insurance: Protecting the Physical Structure

Building insurance covers the bones of your home. This includes everything from the roof and walls to underground pipes and perimeter fences. However, calculating the sum insured involves more than just the market value of the land. A professional assessment must account for “replacement cost,” which includes the often-overlooked expenses of debris removal, demolition, and professional fees for architects or surveyors. Moneysmart’s guide to choosing home insurance provides an excellent starting point for understanding these fundamental requirements. Modern building codes also play a role; if your home was built decades ago, rebuilding it today may require expensive upgrades to meet current fire or energy efficiency standards.

Contents and Personal Valuables: What Lives Inside

When it comes to your possessions, the distinction between “new for old” and “indemnity” value is vital. Indemnity cover only pays out the depreciated value of an item, whereas new for old ensures you can replace a five-year-old laptop with a current equivalent. We encourage our clients to list high-value items separately, such as engagement rings or specialised sporting equipment, to avoid sub-limits that might apply in a standard policy. Portable valuables cover is another layer worth considering, as it extends protection to items like cameras or watches when you leave the house. If you’re unsure how to categorise your assets, our team can help you audit your requirements to ensure nothing is left to chance. Partnering with a home insurance broker sydney families trust ensures that every item, from your sofa to your surfboard, is accounted for with precision.

The Underinsurance Trap: Why Standard Calculators Often Fall Short

Many homeowners fall into the underinsurance trap without even realising it. They trust the automated calculators provided by big insurers, assuming these tools are calibrated for precision. However, these calculators often rely on broad, outdated regional averages that don’t reflect the hyper-inflation we’ve seen in Australian construction. By May 2026, labour shortages and supply chain disruptions have pushed rebuilding costs significantly higher than they were just two years ago. If your sum insured is based on a “tick and flick” quote from 2024, you could be facing a massive financial shortfall after a total loss. Understanding why your home insurance calculator might be leaving you underinsured is a critical first step toward closing that gap.

A seasoned home insurance broker sydney families trust will look beyond simple square-metre rates. We investigate the actual costs of rebuilding your specific home in today’s market conditions. For those seeking absolute certainty, we often discuss “Total Replacement” policy options. Unlike standard “Sum Insured” policies that cap payouts at a fixed dollar amount, Total Replacement covers the actual cost to rebuild the home to its previous standard, regardless of the price. It’s a premium alternative that removes the guesswork from your safety net and ensures your recovery isn’t stalled by a lack of funds. Our comprehensive 2026 Australian guide to insurance home and contents explores these options in greater detail to help you make an informed decision.

The Hidden Costs of Rebuilding

Rebuilding isn’t just about bricks and mortar. There are significant “soft costs” that many standard policies either underestimate or ignore. Debris removal alone can reach tens of thousands of dollars, especially if hazardous materials like asbestos are involved. You must also account for professional fees for architects, surveyors, and the complex process of obtaining council permits. Even “temporary accommodation” limits can be a trap; if a rebuild takes 18 months due to local labour shortages, a standard 12-month accommodation benefit will run out. This leaves you to pay rent out of your own pocket while still servicing a mortgage on a house that doesn’t exist yet.

Market Value vs. Replacement Cost: A Critical Distinction

It’s vital to separate what your home is worth on the real estate market from what it costs to reconstruct. Market value is driven by land location and buyer demand, which is irrelevant to insurance. A home in a more affordable suburb may actually cost more to rebuild than its market value if access is difficult or local building codes are stringent. The sum insured must reflect the cost of a modern equivalent build, not the original purchase price or the current resale value. This distinction is where professional human oversight provides the clarity that an algorithm simply cannot match. Partnering with a home insurance broker sydney residents rely on ensures that your policy is grounded in construction reality, not real estate speculation.

Navigating the Market: The Critical Difference an Insurance Broker Makes

While online comparison sites offer a superficial glimpse into a handful of retail policies, a home insurance broker sydney residents rely on provides a gateway to a much wider landscape. We access wholesale markets and specialised underwriters that aren’t available to the general public, ensuring your property is matched with the most suitable provider rather than just the one with the biggest marketing budget. This professional oversight is particularly important as the industry evolves. For example, with Allianz scheduled to reduce broker commissions to 15% on July 1, 2026, the value of a broker now lies squarely in their ability to provide transparent, high-level advice rather than just facilitating a transaction. We act as your protective mentor, doing the heavy lifting to ensure your policy is as resilient as the home it protects. To understand why this consultative approach consistently outperforms automated systems, explore our detailed analysis of why expert insurance brokers provide more value than automated quotes in 2026.

The PDS Deep-Dive: Finding the Gaps

We don’t just compare prices; we interrogate the contract. Every Product Disclosure Statement (PDS) contains different definitions for events like flood, fire, or storm. What one insurer calls a “storm,” another might classify as “gradual deterioration,” potentially leading to a rejected claim. We perform a deep-dive investigation into these exclusions to ensure you aren’t caught off guard by restrictive fine print. We also identify “sub-limits” on items like jewellery or home office equipment that often sit far below the actual value of your assets. If you want to ensure your contract is as robust as possible, you can reach out to us for a comprehensive policy review that looks beneath the surface of standard retail offerings.

Claims Advocacy: Your Voice When it Matters Most

The true value of a home insurance broker sydney families trust becomes clear during the stress of a major claim. Managing a significant loss directly with a large insurer’s call centre can be an exhausting, impersonal experience. We step in as your professional advocate, leveraging our long-standing relationships with underwriters to ensure your claim is handled fairly and efficiently. We speak the language of the industry, which allows us to push back on technicalities and fight for the outcome you deserve. This partnership provides a sense of relief and stability when you need it most, turning a high-friction process into a managed path toward recovery. You gain the peace of mind that comes from knowing a steady, experienced hand is navigating the complexities on your behalf.

Securing Your Sanctuary: The MyGen Approach to Personalised Protection

We believe your home deserves more than a generic algorithm’s best guess. At MyGen, we’ve built our philosophy on a simple but vital principle: accuracy over automation. While the broader market often rewards speed and volume, we choose a different path. We understand the inherent stress that comes with protecting your most valuable asset, and we position ourselves as a calming, stabilising force in that process. Partnering with a home insurance broker sydney families can actually speak with means moving away from the cold, detached nature of traditional corporate communication. We don’t just facilitate transactions; we build long-term relationships centered on the precision and Suitability of your cover.

The transition from the anxiety of the unknown to the clarity of expert oversight is a journey we take together. Many of our clients come to us feeling frustrated by the “tick and flick” nature of online systems that ignore the unique soul of their property. We validate that frustration by offering a style of service that feels deeply personal and protective. Our goal is to ensure that you feel a sense of relief, knowing that a seasoned expert is doing the heavy lifting on your behalf. By choosing a home insurance broker sydney residents trust for their thoroughness, you are investing in a safety net that is designed to hold up under scrutiny, not just at the point of sale.

A Methodical Path to Peace of Mind

Our risk assessment process is deliberate and logical. We begin by listening to your concerns and validating your specific needs. From there, we conduct a thorough investigation into your property’s unique risk profile, looking beneath the surface of simple postcode data. We’ve seen every possible scenario, and we use that experience to act as a protective mentor for our clients. This human-centric approach ensures that we identify potential gaps before they become problems. You gain access to a steady, experienced hand who values integrity over speed, ensuring that every detail of your policy is grounded in reality.

Taking the Next Step for Your Home

It’s time to move beyond the frustration of generic online forms that leave you questioning your actual level of cover. We invite you to experience a more sophisticated, empathetic way of managing your domestic risk. Starting the conversation with a MyGen specialist is the first step toward a simplified, secure outcome. We take the complexity out of the process, providing you with the certainty that your policy reflects the true value of your sanctuary. Don’t leave your future to chance or a “set and forget” mentality. Organise a personalised home insurance review with MyGen Insurance Brokers today and discover the difference that professional human oversight makes.

Securing Your Future with Professional Precision

Protecting your most valuable asset requires moving beyond the superficial “tick and flick” nature of automated quotes. We’ve explored how the underinsurance trap is fuelled by rising construction costs and why deconstructing the nuances of your policy is essential for true peace of mind. By choosing a home insurance broker sydney families can trust, you ensure that your safety net is built on accurate data and human insight rather than a generic algorithm’s best guess. Our team brings over 20 years of industry experience to every consultation, focusing on personalised risk assessments that reflect the reality of your property. We don’t just set up a policy; we provide dedicated claims advocacy and support when you need it most. You deserve the certainty that your sanctuary is shielded by a strategy as unique as the home itself.

Let MyGen Insurance Brokers find the right protection for your home

Take the first step toward a more secure future today. We are here to do the heavy lifting, ensuring you can rest easy knowing your home is in safe, experienced hands.

Frequently Asked Questions

What is the difference between home and homeowners insurance?

Home and homeowners insurance are generally used interchangeably in the Australian market to describe the protection of a private residence. Specifically, a homeowners policy is designed for owner-occupiers, combining building cover with public liability to protect your legal interests. It ensures that both the physical structure and your personal liability as a resident are shielded from financial loss.

How is the “sum insured” calculated for an Australian home?

The sum insured is calculated by estimating the total cost to rebuild your home from scratch at current 2026 construction rates. This includes materials and labour, but you must also factor in debris removal and professional fees for architects or surveyors. It’s a common mistake to use the market value of your land, which often leads to significant coverage gaps during a claim.

Does standard home insurance cover flood and bushfire?

Most Australian policies include bushfire as a standard defined event, but flood coverage varies significantly between providers. Some insurers include flood automatically, while others offer it as an optional extra with very specific definitions regarding “rising water” versus “stormwater runoff.” A home insurance broker sydney families trust will interrogate these definitions to ensure your specific location is properly protected.

Why should I use an insurance broker instead of going direct?

Using a home insurance broker sydney residents rely on gives you access to professional advocacy and wholesale markets that aren’t available to the general public. While direct insurers use automated systems that prioritise speed, a broker performs a deep dive into the fine print. This human-centric approach ensures your policy is a bespoke strategy rather than a generic transaction.

What is “Total Replacement” cover and is it worth it?

Total Replacement cover is a premium option that pays the actual cost to rebuild your home to its previous size and quality, even if it exceeds the sum insured limit. It’s particularly valuable as construction costs and labour shortages continue to fluctuate across New South Wales. This option removes the risk of underinsurance and provides absolute certainty during the stress of a total loss claim.

How often should I review my home and contents policy?

You should review your home and contents policy at least once every twelve months during your renewal period. It’s also vital to update your cover immediately after finishing renovations, installing solar panels, or purchasing high-value items like specialised sporting equipment. Regular reviews ensure your safety net keeps pace with your changing lifestyle and the current economic climate.

Are my home office items covered under a standard home policy?

Standard home policies usually provide limited cover for home office equipment, often with a low sub-limit that may not reflect the true value of your tech. If you run a business from home or own expensive specialised equipment, these standard limits are rarely enough to cover a total loss. We often recommend specifying these items separately to ensure they are fully protected against theft or accidental damage.

What happens if I accidentally underinsure my property?

If you accidentally underinsure your property, you’ll be responsible for paying the difference between your insurance payout and the actual rebuild cost. In some cases, insurers apply an “averaging” clause, where they reduce your claim payout by the same percentage you were underinsured. This can turn a manageable repair into a significant financial burden that stalls your recovery process for years.

Leave a Reply