What if the “cheap” online quote you secured last year is actually the most expensive mistake your business will ever make? We understand the frustration of watching commercial reconstruction costs climb by over 4% while you’re stuck on hold with an automated call centre that doesn’t know your local area. It’s unsettling to feel like your commercial property insurance has become a generic box-ticking exercise rather than a genuine shield for your assets. You aren’t alone in worrying about the “cyber-physical” gap or whether your current limits would actually cover a total loss in the current economy.

We believe you deserve a partner who looks beneath the surface to identify the specific risks your business faces in 2026. This article will show you how to move beyond “basic” cover to find a solution that’s truly suitable for the modern landscape. We’ll break down the latest trends in market stabilisation, explain how to manage inflation-driven limit increases, and provide a clear roadmap to ensure your business is protected against both physical disasters and emerging digital threats.

Key Takeaways

- Learn why a 2024 valuation is likely obsolete in today’s economy and how to accurately calculate replacement costs to avoid being underinsured.

- Discover the “cyber-physical” gap in standard commercial property insurance and why smart building systems require a more sophisticated approach to protection.

- Understand why automated “quote-and-bind” systems often miss critical vulnerabilities that only a manual, consultative risk assessment can uncover.

- Gain the clarity needed to transition from “cheap” generic cover to a suitable policy that provides genuine peace of mind and long-term security.

The Shifting Landscape of Commercial Property Insurance in 2026

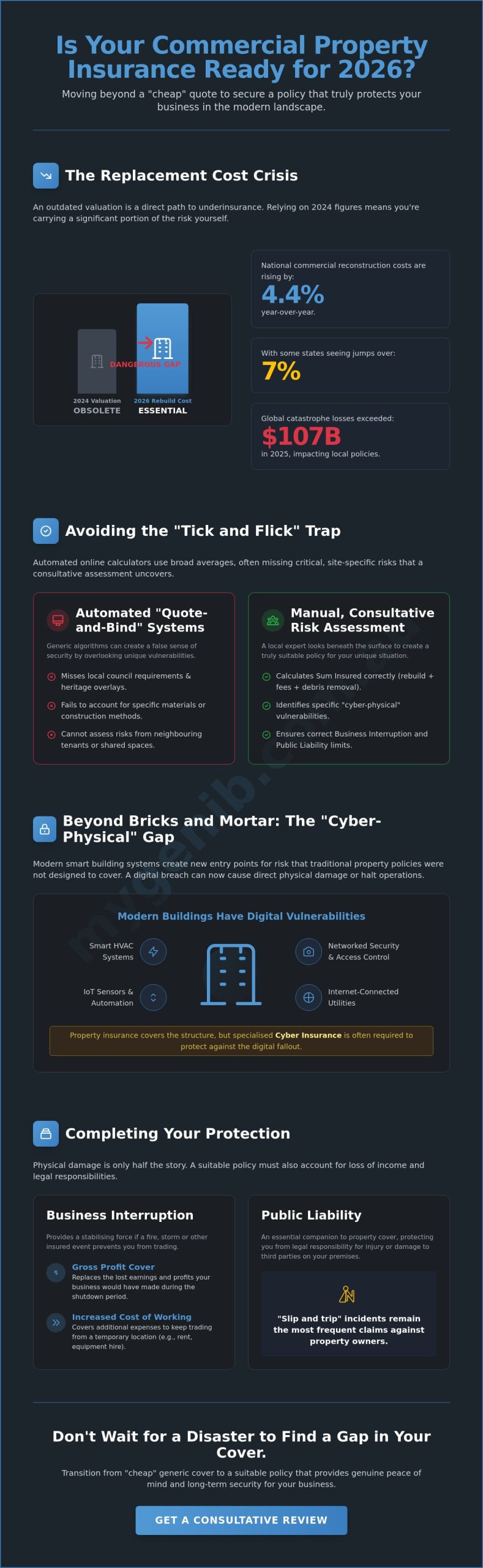

At its heart, commercial property insurance acts as a comprehensive shield for your physical assets, stock, and the vital continuity of your operations. It provides the financial foundation that allows a business to recover when the unexpected occurs. However, we’re seeing a growing “Replacement Cost Crisis” where valuations from just two years ago no longer reflect the reality of 2026. With national commercial reconstruction costs rising by 4.4% year-over-year, and some states seeing jumps over 7%, a 2024 valuation is likely obsolete. Relying on outdated figures means you’re carrying the risk yourself. Many businesses bundle these covers into a Business Owner’s Policy (BOP), but even these packages require a deep dive to ensure they match the current economic climate. Australian climate trends have also forced a shift in policy wording, as insurers react to global catastrophe losses that exceeded $107 billion in 2025. A “set and forget” mentality is no longer viable; it’s a path straight toward dangerous underinsurance.

Why Automated Online Calculators Often Fall Short

The “Tick and Flick” trap is a common pitfall where generic algorithms miss unique, site-specific risks that a local expert would spot instantly. These tools often use broad averages that fail to account for the intricate details of your specific premises. We’ve observed a similar pattern in residential markets, where home insurance calculators often underestimate costs by ignoring local council requirements or heritage overlays. In 2026, your Sum Insured must represent the total cost to rebuild your property to current Australian building standards, including all professional fees and debris removal, rather than just the market value of the building.

The Rise of Business Interruption as a Core Component

Physical property damage is often only half the story. If a fire or storm prevents you from trading for six months, the loss of income can be more devastating than the damage itself. It’s vital to distinguish between “Gross Profit” cover, which replaces lost earnings, and “Increased Cost of Working” cover, which pays for the additional expenses required to keep your business running from a temporary location. We help you look beneath the surface to ensure your commercial property insurance accounts for both, providing a stabilizing force when your business needs it most.

Beyond Bricks and Mortar: Identifying Modern Vulnerabilities

We often think of property damage as something you can see and touch, like a cracked wall or a flooded warehouse. However, the rise of “cyber-physical” risks in 2026 has blurred the lines between digital security and physical safety. Modern smart building systems, including HVAC, security cameras, and IoT sensors, have created new entry points for risk that traditional policies weren’t designed to handle. A breach in these systems doesn’t just result in lost data; it can lead to physical damage or a total halt in operations. Engaging in proactive risk management means looking beyond the physical structure to identify these hidden digital gateways.

A common misconception we encounter is the belief that older buildings are immune to these modern threats. It’s a dangerous assumption. Even if your premises lacks integrated smart technology, your security systems, point-of-sale terminals, and internet-connected utilities still bridge the gap between the physical and digital worlds. While your commercial property insurance covers the structure, a specialised cyber insurance in Australia is often required as a companion to protect against the fallout of digital interference. We’ve seen how a single digital vulnerability can stop a business in its tracks, proving that modern protection must be multi-layered.

The Hidden Risks of Shared Spaces and Strata

Navigating the complexities of tenant and landlord responsibilities in commercial hubs requires a meticulous eye. In shared spaces, one tenant’s high-risk profile can inadvertently impact the insurability of the entire building. If a neighbouring business stores hazardous materials or lacks proper security, your own commercial property insurance terms may be affected. We work to clarify these boundaries, ensuring you aren’t left exposed by someone else’s oversight.

Public Liability: The Essential Companion

Your physical premises are inextricably linked to your legal responsibilities toward anyone who steps onto the property. This is why public liability insurance is an essential companion to property cover. Despite all the technological shifts, “slip and trip” incidents remain the most frequent claims against property owners. Ensuring your cover is suitable for your specific foot traffic can provide the relief you need to focus on your daily operations. If you’re unsure where your property cover ends and your liability begins, we can help you audit your current business insurance to find the gaps.

Securing Your Investment: The Consultative Path to Protection

In a market where many providers prioritise speed over precision, we choose to focus on depth. While an automated system might offer a “quick” quote in minutes, it often fails to see the nuances of your specific operation. Securing the right commercial property insurance isn’t about finding the fastest transaction; it’s about building a partnership with a protective mentor who does the heavy lifting for you. We move from “skimming” the surface to a “deep dive” investigation, ensuring every asset and vulnerability is accounted for before a policy is even drafted. This methodical approach provides the certainty that your business is truly protected, especially as the insurance market begins to stabilise after years of volatility.

The 4-Step Risk Review Process

Our investigative approach follows a logical, four-step path designed to turn confusion into clarity:

- Step 1: Physical Site Inspection and Asset Valuation. We conduct a thorough “Deep Dive” to ensure your replacement costs match current 2026 reconstruction prices.

- Step 2: Operational Vulnerability Mapping. We look beyond the walls to identify risks in business interruption and the emerging cyber-physical gap.

- Step 3: Market Tendering. We search for the right underwriter who understands your specific industry, rather than just chasing the cheapest premium.

- Step 4: Ongoing Advocacy. Our work doesn’t end at the renewal; we provide constant claims support and annual reviews to keep your cover relevant.

The Broker Advantage in a Complex Market

Having a seasoned hand to guide you makes all the difference when the unexpected occurs. Working with insurance brokers gives you a dedicated advocate who stands in your corner during the claims process, ensuring you aren’t just another number in a call centre queue. While a direct insurer represents their own interests and products, an Authorised Representative is a licensed professional who acts on your behalf to negotiate terms and ensure your commercial property insurance actually performs when you need it most. This relationship-first model turns a high-friction experience into one that feels managed, secure, and deeply personal.

Protecting Your Business Legacy Beyond 2026

Protecting your business assets in 2026 requires a deliberate shift from passive coverage to active, informed risk management. We’ve explored how rapidly rising reconstruction costs and the emerging “cyber-physical” gap have fundamentally changed what it means to be fully covered. It’s clear that a generic, automated policy simply cannot provide the depth of security your specific operation demands. Relying on a “tick and flick” system often leads to the very underinsurance traps we’ve discussed, leaving your hard-earned legacy at risk.

At MyGen, we take this responsibility personally and treat your business as if it were our own. Led by Anthony Simpson with over 20 years of industry experience, our team acts as a protective mentor to guide you through these evolving challenges. As a Corporate Authorised Representative of the Community Broker Network, we reject superficial assessments in favour of a thorough, investigative process. We’re here to do the heavy lifting, ensuring your commercial property insurance is a precise fit for your unique risks. You don’t have to navigate this complex landscape alone. Organise a personalised risk consultation with MyGen today and experience the relief that comes with genuine professional advocacy. We look forward to helping you build a more secure and stable future.

Frequently Asked Questions

Is commercial property insurance compulsory in Australia?

No, it isn’t legally mandated by the government in the same way as Workers’ Compensation or CTP insurance. However, you’ll find that most commercial mortgage lenders and landlords require it as a condition of your finance or lease agreement. We view it as a fundamental safety net that protects your business from financial ruin if a major event occurs, providing the stability you need to operate with confidence.

Does commercial property insurance cover my tenants’ belongings?

Generally, no. A landlord’s policy is designed to protect the physical building and any permanent fixtures, while tenants are responsible for insuring their own stock, furniture, and fit-outs. It’s a common area of confusion in shared commercial hubs that can lead to disputes during a claim. To see how these policies are structured to protect your investment, you can learn more about WS Insurance Brokers and their landlord-specific cover. We recommend that both parties clearly define these boundaries in the lease to ensure there aren’t any gaps in your commercial property insurance strategy.

How much does commercial property insurance cost in 2026?

Pricing in 2026 is highly individual and depends on your specific industry, location, and the age of your building. While some sectors might see lower premiums due to low-risk profiles, higher-risk industries often face higher costs due to the nature of their operations. Factors like your claims history and the accuracy of your replacement cost valuations play a major role in the final figure. We focus on finding a suitable rate that reflects your actual risk rather than just providing a generic, automated estimate.

What is the difference between building insurance and commercial property insurance?

Building insurance typically focuses only on the physical structure, whereas commercial property insurance is a broader solution that can include your contents, stock, and business interruption. It acts as a more comprehensive shield for your entire operation rather than just the bricks and mortar. This distinction is vital because a structure-only policy won’t help you recover lost income if a fire or storm forces you to stop trading for several months while repairs are carried out.

Leave a Reply