What if the most dangerous part of your business isn’t what you do, but what you sell? Many Australian business owners believe that if they didn’t manufacture a product themselves, they aren’t on the hook if it fails. However, under the Australian Consumer Law, the responsibility often lands on the person who put the item into the customer’s hands. We understand it’s exhausting to keep up with shifting regulations like the Competition and Consumer Amendment (Unfair Trading Practices) Bill 2026, especially when you’re focused on daily operations. It’s natural to feel a sense of dread when considering how a single faulty batch could lead to a compensation claim that threatens your entire livelihood.

You probably wonder if you really need separate product liability insurance if you already have public liability. While they’re often bundled together, they address distinct risks that require a methodical approach to manage. We’re here to help you distinguish between the two and identify the hidden vulnerabilities within your specific supply chain. This guide will clarify your legal exposure and show you how to ensure your policy matches your actual business activities. You deserve the peace of mind that comes from knowing a seasoned professional has helped you secure your future.

Key Takeaways

- Clearly distinguish between public liability accidents and the unique risks that arise once a product leaves your control.

- Recognise the extent of your legal obligations under the latest Australian Consumer Law updates to avoid unexpected financial exposure.

- Identify why a “tick and flick” automated quote might leave significant gaps in your product liability insurance and how a consultative approach offers better protection.

- Uncover the specific types of personal injury and property damage claims that can stem from faulty goods or supply chain failures.

- Learn how to align your coverage with your specific business activities to achieve genuine peace of mind.

Product Liability vs Public Liability: Clearing the Confusion

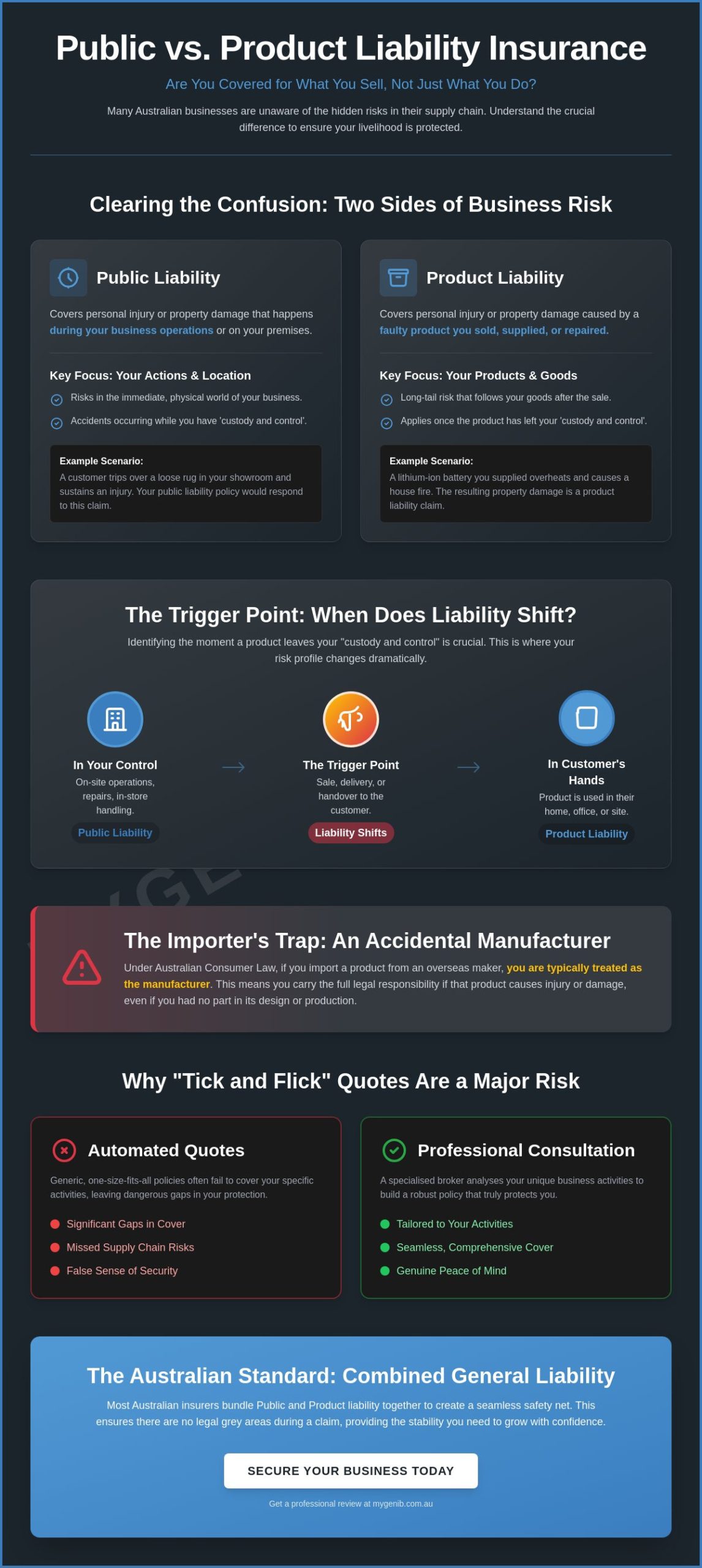

Understanding the difference between these two forms of protection is vital for any Australian business owner. Public liability typically handles the immediate, physical world of your operations. If a customer trips over a loose rug in your showroom or an employee accidentally knocks over a ladder on a job site, your public liability cover is there to catch you. It focuses on the risks inherent in your day-to-day activities and the physical spaces you occupy. We know how much effort you put into maintaining a safe environment, but accidents can happen in the blink of an eye.

Conversely, Product liability is the area of law that deals with the consequences of what you sell once it is out in the world. While public liability protects you while the work is being done, product liability insurance steps in the moment that item leaves your hands. If a faulty lithium-ion battery you supplied catches fire in a customer’s home at 2:00 am, the resulting property damage is a product liability issue, not a public one. It is about the long-tail risk that follows your goods long after the transaction is complete.

To better understand this concept, watch this helpful video:

The Trigger Point: When Does Liability Shift?

In Australian insurance policies, this shift often hinges on the concept of “custody and control.” As long as you or your staff are handling the item, it falls under your public liability. However, the second that product is sold, delivered, or the repair is completed and handed back to the client, the trigger point moves. Identifying this moment is crucial because it defines where your exposure begins. For an e-commerce store, this might be the moment a package is collected by a courier; for a mechanic, it is when the keys are handed back to the car owner. We help you map out these moments so there are no gaps in your safety net.

Why “Combined Liability” is the Australian Standard

We find that most insurers in Australia now bundle these together as a “Combined General Liability” policy. This isn’t just for convenience; it’s designed to create a seamless safety net for SMEs. Because the line between a service and a product can sometimes blur, having both ensures you aren’t left in a legal grey area during a claim. We make sure your product liability insurance wording is robust enough to cover both personal injury and property damage, providing the stability you need to grow your business with confidence. It is about looking beneath the surface to ensure your specific business activities are actually protected.

What Does Product Liability Actually Cover?

At its core, product liability insurance is designed to protect your business when a product fails to perform safely. This isn’t just about a simple refund; it’s about the financial fallout from personal injury or significant property damage. If a customer suffers a severe allergic reaction due to an unlabelled ingredient or a structural failure in a piece of equipment causes a workplace accident, the costs can be devastating. We’ve seen how these claims can spiral, which is why a policy that covers both damages and the substantial legal costs required to defend your reputation is essential. Even if a claim is ultimately found to be baseless, the expense of a legal defence can bankrupt an unprotected firm.

The Australian Competition and Consumer Commission (ACCC) sets high standards for a supplier’s duty of care. When legal disputes arise, there are several causes of action available to claimants under the Australian Consumer Law. We help you navigate these complexities, turning a high-friction legal environment into a managed risk that allows you to focus on growth. It’s about providing a stabilizing force when you feel most vulnerable.

The Importer’s Trap: Why You Might Be Considered a “Manufacturer”

Many Australian retailers don’t realise they’re walking into a trap when they source goods from overseas. If you import a product from a factory in another country, Australian law typically treats you as the manufacturer. This means if the original maker is unreachable or outside our jurisdiction, the legal and financial responsibility sits squarely on your shoulders. It’s a heavy burden. We take the time to look beneath the surface of your business model to ensure your business insurance reflects your actual level of risk, especially if you’re the primary point of contact for foreign goods.

Design Defects vs. Manufacturing Faults

Every product has two main failure points. A design defect means every single unit is fundamentally unsafe, whereas a manufacturing fault might only affect a specific batch or a one-off assembly error. Whether it’s a deep-seated design flaw or a simple mistake on the factory floor, the impact on your business remains the same. Your broker needs to understand these nuances to provide accurate advice. We pride ourselves on being deep-divers who investigate your specific role in the supply chain to ensure your product liability insurance is fit for purpose and leaves no room for uncertainty.

Why Automated Quotes Often Miss the Mark for Product Risk

Speed is often the enemy of security. While the promise of a five-minute online quote is tempting for a busy business owner, this “tick and flick” approach can leave your business with dangerous coverage gaps. Algorithms are designed for the average, but your business isn’t average. A generic form won’t ask about obscure product components or whether your goods are intended for a high-risk end-use. If these details are missed, your product liability insurance might fail you exactly when you need it most. We’ve seen how a single overlooked detail in a supply chain can lead to a rejected claim, turning a supposed saving into a massive financial burden.

Having a seasoned expert in your corner provides a level of protection that no software can replicate. When a claim arises, the legal landscape becomes incredibly complex very quickly. A broker acts as your protective mentor, doing the heavy lifting and navigating the investigation process on your behalf. This partnership allows you to move from a state of constant anxiety about “what if” to a state of calm, knowing that your livelihood is managed by someone who understands the stakes. For professionals whose work involves advice or expertise, this same principle applies to professional indemnity insurance for Australian professionals, which addresses the distinct risks that arise from the services you deliver rather than the products you supply.

The Consultative Difference: Looking Beneath the Surface

We prioritise depth and precision over the hollow speed of an automated quote. Our methodical approach involves a deep-dive into your operations to uncover the risks that a simple system would overlook. By conducting a manual review of your contracts and supplier agreements — including understanding what is an indemnity clause and how it can shift financial risk onto your business — we ensure your policy is a true reflection of your risk profile. You can learn more about why expert insurance brokers provide more value than automated quotes in 2026 through our detailed analysis of the current market.

Securing Your Outcome: The Path to Peace of Mind

Securing your business shouldn’t feel like a transaction; it should feel like a partnership. To ensure your protection is robust and fit for purpose, start by identifying every hand that touches your product before it reaches the customer. We recommend reviewing the complete guide to business insurance in Australia to see how your different covers work together. When you’re ready for a policy that offers genuine certainty, let’s have a personal conversation. We’re here to ensure your product liability insurance is as resilient as the business you’ve built.

Securing Your Business Legacy for the Long Term

Managing the hidden risks of your supply chain is no longer a task you can leave to chance or an unfeeling algorithm. We’ve explored how the critical distinction between public and product risk hinges on the moment of handover, and why importing goods often makes you a manufacturer in the eyes of Australian law. Relying on a generic online form can leave you exposed to claims that threaten everything you’ve built. Protecting your livelihood requires a deep-dive into the specifics of what you sell and how you sell it.

At MyGen Insurance Brokers, we believe in a methodical, human-centric approach to product liability insurance. Led by Anthony Simpson, who brings over 20 years of industry experience to every client relationship, we specialise in Australian business risk management. We move beyond “tick and flick” quotes to provide a personalised consultative experience that truly reflects your unique operations. When you’re ready to trade uncertainty for genuine peace of mind, we invite you to Speak with a MyGen Broker for a Personalised Risk Assessment. Let’s work together to ensure your future is as secure as it is successful. Your hard work deserves the protection of a steady, experienced hand.

Frequently Asked Questions

Is product liability insurance compulsory for Australian businesses?

No, product liability insurance isn’t legally mandated for every Australian business, but it’s often a contractual necessity. Most major retailers and distributors won’t even consider a partnership without proof of cover. Even without a contract, the Australian Consumer Law places a heavy burden on suppliers, making this protection a fundamental part of a professional risk management strategy for anyone in the supply chain.

Does product liability cover the cost of a product recall?

Typically, a standard policy won’t cover the logistical nightmare of a product recall. While the insurance handles the fallout from injury or property damage, the costs of notifying the public, shipping faulty goods back, and disposing of them usually require a separate recall extension. We recommend looking beneath the surface of your standard policy to see if this additional security is a priority for your specific business model.

I am a sole trader providing a service; do I still need product liability?

Even as a service provider, you face exposure if you supply or install any physical components. If you’re a plumber who installs a faulty valve or a technician who provides a specific part as part of your package, you can be held liable if that item fails. It’s a common anxiety for sole traders, but having the right cover ensures that a single faulty part doesn’t bankrupt your personal finances or ruin your professional reputation. If your work also involves providing advice or expertise, you may want to explore professional indemnity insurance tailored to Australian professionals to address that separate but equally important area of risk.

How much does product liability insurance typically cost in 2026?

Pricing for product liability insurance isn’t a one-size-fits-all figure and depends heavily on your specific business activities. Factors like your annual turnover, the volume of goods you sell, and whether you import products from overseas all play a role in determining your premium. We avoid generic estimates in favour of a methodical review, ensuring your premium matches the actual depth of your risk rather than an arbitrary industry average.

Leave a Reply