A local business owner recently discovered that a single moment of inattention on a job site could lead to a legal claim larger than their entire annual turnover. For many Australian entrepreneurs, the anxiety isn’t just about the accident itself; it’s the crushing weight of legal jargon and the worry that a generic policy won’t actually stand up when it’s needed most. You likely feel that protecting your livelihood should be straightforward, yet when you’re trying to figure out what is public liability insurance, you’re often met with automated forms that don’t understand the specific risks of your trade.

We believe you deserve better than a “best guess” approach to your security. This guide functions as a clear roadmap to help you move from a state of uncertainty to one of complete confidence by showing you how to align your cover with your actual daily operations. We’ll explore the critical differences between public and product liability, look at why the Insurance Council of Australia is currently pushing for urgent civil liability reforms, and help you determine the level of protection that truly fits your business size and sector. Our goal is to ensure you feel protected by a policy that is as diligent and thorough as you are.

Key Takeaways

- Learn exactly what is public liability insurance and how it acts as a vital financial buffer against the unpredictable costs of third-party injury or property damage claims.

- Discover why a robust policy covers far more than just settlements, providing the essential legal and investigative support needed to defend your business’s reputation and livelihood.

- Understand the concept of “duty of care” in an Australian context to better identify the specific operational risks that could lead to significant financial exposure.

- See why standard cover limits shouldn’t be a “best guess” and how a tailored approach helps you determine a level of protection that reflects your daily reality.

- Learn to look beneath the surface of generic policies to ensure your cover is organised around your specific trade rather than a one-size-fits-all template.

Understanding Public Liability Insurance: Your Business Safety Net

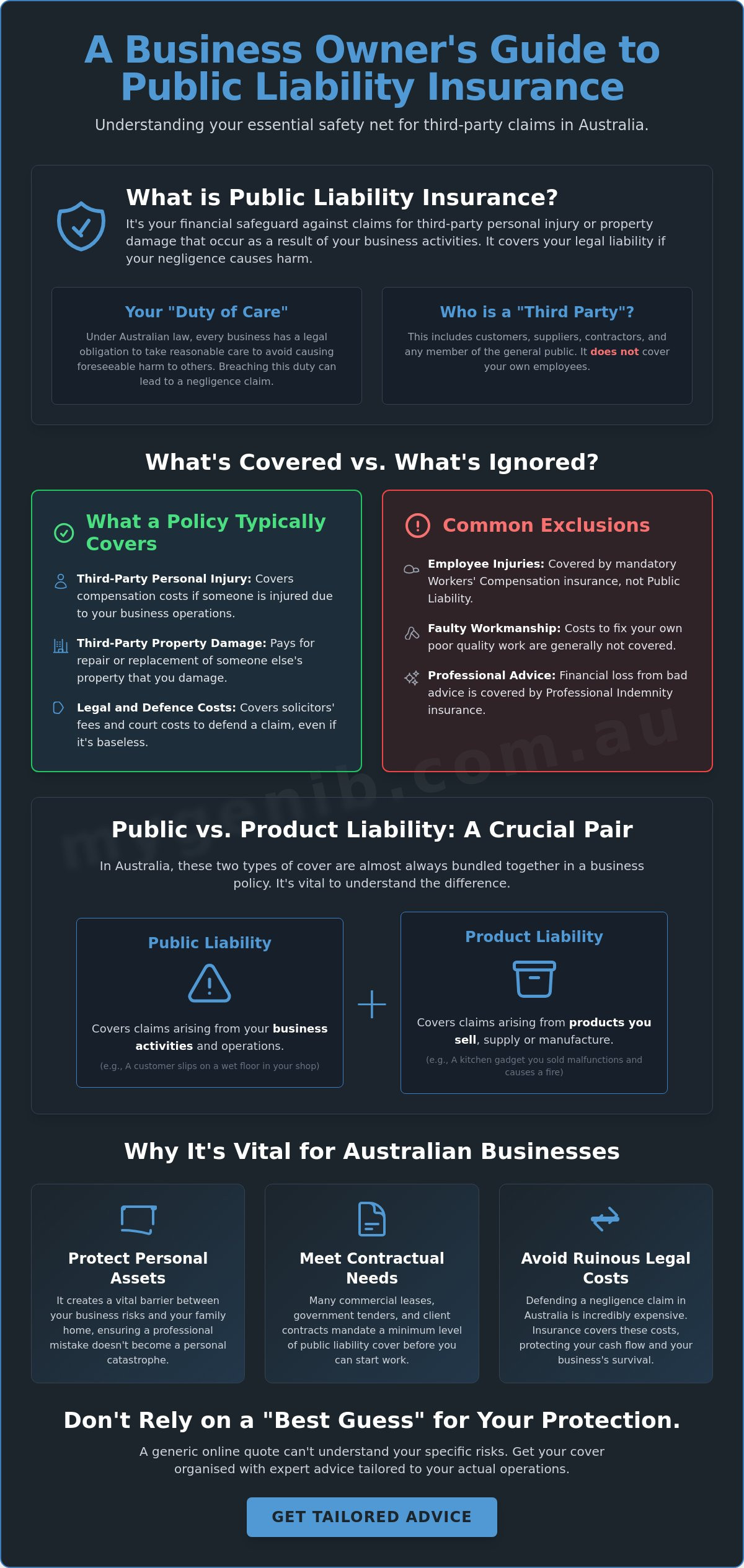

At its heart, Public liability is about protection against the unexpected. If a customer trips over a loose cable in your shop or a delivery driver is injured by a falling pallet at your warehouse, you’re legally responsible for the fallout. This insurance covers the financial loss resulting from your legal liability for third-party injury or property damage. It’s the difference between a minor setback and a business-ending financial crisis.

In Australia, every business operator has a “Duty of Care” to ensure their actions don’t cause harm to others. When this duty is breached through negligence, it triggers a claim. Understanding what is public liability insurance requires looking at these daily risks through the lens of Australian Consumer Law and the common law principles of negligence, which set high standards for public safety.

To better understand this concept, watch this helpful video:

It’s vital to clarify who these “third parties” actually are. They include your customers, suppliers, and any member of the public who interacts with your business. However, your own team members are a different story; injuries to employees are covered by workers’ compensation, not public liability.

By 2026, the lines between home and work have blurred significantly. If you run a consultancy or an online store from your spare room, don’t assume your home insurance has your back. Most standard residential policies specifically exclude business-related incidents, leaving home-based entrepreneurs exposed if a courier slips on their driveway.

Why is it Vital for Australian Small Businesses?

Litigation in Australia is increasingly sophisticated and expensive. For a sole trader, the cost of defending a single negligence claim can quickly outstrip their savings, especially as the Insurance Council of Australia continues to monitor rising claim costs across the country.

Beyond the legal risks, having cover is often a ticket to entry. Most commercial leases and government contracts now mandate a minimum level of business insurance before you can even sign on the dotted line. It’s a standard requirement that ensures all parties are protected if something goes wrong on-site.

Most importantly, it provides a layer of separation between your professional risks and your personal life. It ensures your family home and personal assets aren’t the collateral damage of a professional accident, giving you the peace of mind to focus on growth rather than worst-case scenarios.

What Does Public Liability Cover (and What Does It Ignore)?

Understanding the actual scope of your protection is the first step toward true peace of mind. Most people asking what is public liability insurance expect it to cover a simple slip and trip, but a robust policy is built on three distinct pillars: personal injury, property damage, and advertising injury. This third pillar is often overlooked, yet it protects your business if you’re accused of libel, slander, or copyright infringement in your marketing materials.

Your cover isn’t just about the final settlement paid to a claimant. According to the Insurance Council of Australia, the investigative and legal costs required to defend a claim can be staggering, even if you’ve done nothing wrong. A professional policy handles these expenses, ensuring your cash flow isn’t drained by solicitors’ fees while you’re trying to clear your name. This protection travels with you, whether you’re operating from your own shopfront or working on-site at a client’s property.

The Crucial Link Between Public and Product Liability

In the Australian market, these two are almost always bundled together in what we call “Business Pack” policies. Product liability covers you if a product you sell, supply, or even give away causes injury or damage. Imagine you sell a kitchen gadget that malfunctions and causes a fire; even if you didn’t manufacture the item, you could still be held liable as the supplier. To get a deeper look at this relationship, you can read our guide on Product Liability vs Public Liability: Know the Difference.

Common Traps in Standard Policies

Not all policies are created equal. Many “tick-and-flick” online forms fail to account for the nuances of your specific trade. You might find your cover has restrictive sub-limits or excludes work in high-risk environments like mines, airports, or railway stations. If you’re unsure if your current policy has these gaps, it’s worth having an expert review your business insurance to ensure your protection is as deep as it needs to be. Remember, standard cover often ignores professional advice, which requires separate professional indemnity, and intentional damage is never covered.

Organising the Right Cover: Moving Beyond Automated Quotes

Choosing a cover limit shouldn’t be a game of guesswork or a default selection. While $5 million, $10 million, and $20 million are the standard benchmarks in the Australian market, these figures don’t automatically account for the unique pressure points of your specific trade. When you truly grasp what is public liability insurance, you realise it’s not just a contract requirement to be ticked off. It’s a calculated response to your actual financial exposure in a litigious environment.

The “instant quote” model often prioritises speed over suitability, leaving many business owners dangerously underinsured. We favour a consultative approach that focuses on the depth of risk discovery. This methodical process ensures your Certificate of Currency is backed by a policy that actually understands your work. The Australian government’s definition of public liability insurance notes that it’s often compulsory for certain occupations, but the quality of that protection depends entirely on how well the policy is aligned with your daily reality.

The Value of an Australian Insurance Broker

A broker is more than a salesperson; they’re your advocate when things go pear-shaped. While an automated system might leave you to navigate a complex claim alone, we stand with you to ensure the underwriter meets their obligations. This partnership allows us to tailor a business insurance package that evolves as your firm grows. With over 20 years of experience, Anthony Simpson brings a seasoned, protective perspective to the risk assessment process, identifying potential hazards that a “skimming” approach would inevitably miss. To understand how the right professional can transform your risk management strategy, explore our detailed guide on business insurance brokers and how to find the right advocate for your Australian enterprise.

Next Steps: How to Conduct a Risk Review

Before you commit to a renewal, take a moment to look at your business from the outside in. Gather your annual turnover figures, staff numbers, and any specific contract requirements from your clients or landlords. It’s tempting to focus solely on the premium price, but the true value lies in the quality of the policy wording. If you’re ready for a deeper level of protection, you can organise a personalised risk consultation with MyGen today. We’ll help you turn the complex question of what is public liability insurance into a clear, managed strategy for your business’s future.

Securing Your Business Future with Confidence

Building a resilient business in Australia requires more than just hard work; it demands a clear-eyed understanding of the risks that sit just beneath the surface of your daily operations. We’ve explored how a tailored policy protects you from the complexities of negligence claims and why a simple “tick and flick” approach often leaves dangerous gaps in your cover. By now, your perspective on what is public liability insurance should have shifted from seeing it as a mere expense to valuing it as a sophisticated shield for your personal and professional assets.

You don’t have to navigate these choices alone. As members of the Community Broker Network, we take a deep-dive approach to your security that automated forms simply can’t match. Led by Anthony Simpson, who brings over 20 years of industry experience to every risk assessment, we’re here to help you move from confusion to complete certainty. We invite you to organise a consultative risk review for your business with MyGen today. Let’s work together to ensure your livelihood is protected by a policy that’s as diligent and dedicated as you are.

Frequently Asked Questions

Is public liability insurance compulsory in Australia?

Public liability cover isn’t legally mandatory for every single business type in Australia, but it’s often a practical necessity for daily operations. Many industry bodies require it for trade licensing, while landlords and local councils typically mandate a minimum level of cover before you can sign a lease or set up a stall. If you’re tendering for government work or large corporate contracts, you’ll almost certainly need to provide proof of insurance to be considered.

How much public liability insurance do I need for my business?

The amount of cover you require depends heavily on your specific industry and the contractual obligations you’ve agreed to. While $10 million is the most common limit for small businesses, certain high-risk trades or high-traffic environments may require $20 million or more to satisfy safety standards. We focus on looking beneath the surface of your business to ensure your limit reflects the actual scale of your potential exposure rather than a generic industry average.

Does public liability insurance cover my employees?

No, this insurance is designed specifically for third-party claims and does not provide protection for injuries sustained by your own employees. When you’re researching what is public liability insurance, it’s important to distinguish it from workers’ compensation, which is a separate, compulsory requirement for employers in every Australian state and territory. This policy focuses on protecting your livelihood from claims made by customers, couriers, or members of the public.

Can I get public liability insurance as a sole trader?

Sole traders can certainly access this cover, and it’s arguably even more critical for them than for larger firms. Because a sole trader is legally the same entity as their business, your personal assets like your family home and car are at risk if a claim is made against you. Organising a tailored public liability insurance sole trader policy ensures that a single professional mishap doesn’t lead to personal financial ruin, giving you a stabilising force to lean on as you grow.

Leave a Reply